Page 38 - FS-Q2-2023-EN

P. 38

AL-MAZAYA HOLDING COMPANY - K.S.C. (PUBLIC)

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2023

(All amounts are in Kuwaiti Dinar)

- Leases

Key sources of estimation uncertainty in the application of IFRS 16 include, among others, the following:

• Estimation of the lease term.

• Determination of the appropriate rate to discount the lease payments.

• Assessment of whether a right-of-use asset is impaired.

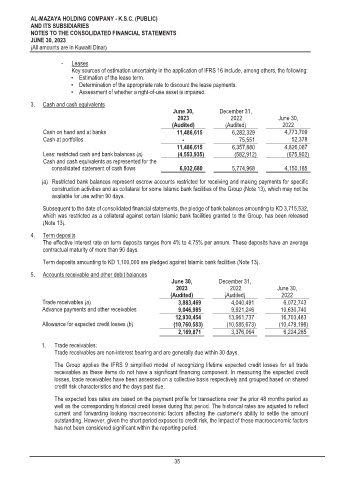

3. Cash and cash equivalents

June 30, December 31,

2023 2022 June 30,

(Audited) (Audited) 2022

Cash on hand and at banks 11,486,615 6,282,329 4,773,709

Cash at portfolios - 75,551 52,378

11,486,615 6,357,880 4,826,087

Less: restricted cash and bank balances (a) (4,553,935) (582,912) (675,902)

Cash and cash equivalents as represented for the

consolidated statement of cash flows 6,932,680 5,774,968 4,150,185

(a) Restricted bank balances represent escrow accounts restricted for receiving and making payments for specific

construction activities and as collateral for some Islamic bank facilities of the Group (Note 13), which may not be

available for use within 90 days.

Subsequent to the date of consolidated financial statements, the pledge of bank balances amounting to KD 3,715,532,

which was restricted as a collateral against certain Islamic bank facilities granted to the Group, has been released

(Note 13).

4. Term deposits

The effective interest rate on term deposits ranges from 4% to 4.75% per annum. These deposits have an average

contractual maturity of more than 90 days.

Term deposits amounting to KD 1,100,000 are pledged against Islamic bank facilities (Note 13).

5. Accounts receivable and other debit balances

June 30, December 31,

2023 2022 June 30,

(Audited) (Audited) 2022

Trade receivables (a) 3,883,469 4,040,491 6,072,743

Advance payments and other receivables 9,046,985 9,921,246 10,630,740

12,930,454 13,961,737 16,703,483

Allowance for expected credit losses (b) (10,760,583) (10,585,673) (10,479,198)

2,169,871 3,376,064 6,224,285

1. Trade receivables:

Trade receivables are non-interest bearing and are generally due within 30 days.

The Group applies the IFRS 9 simplified model of recognizing lifetime expected credit losses for all trade

receivables as these items do not have a significant financing component. In measuring the expected credit

losses, trade receivables have been assessed on a collective basis respectively and grouped based on shared

credit risk characteristics and the days past due.

The expected loss rates are based on the payment profile for transactions over the prior 48 months period as

well as the corresponding historical credit losses during that period. The historical rates are adjusted to reflect

current and forwarding looking macroeconomic factors affecting the customer’s ability to settle the amount

outstanding. However, given the short period exposed to credit risk, the impact of these macroeconomic factors

has not been considered significant within the reporting period.

35